Now that we finally have some legislative certainty around various aspects of paying a Transition to Retirement Income Stream (TRIS), the Australian Taxation Office (ATO) has issued Guidance Note, GN 2019/1 that provides guidance on the changes to transition-to-retirement income streams that commenced from 1 July 2017.

How they apply within the APRA-regulated environment as a ‘product’ versus how they operate within SMSFs can be argued to be very different, however the ATO’s guidance defends this view that once a TRIS is established it always remains a TRIS (unless the income stream ceases).

TRIS in the retirement phase

The TRIS in retirement phase concept is predominantly a result of public offer fund products, as opposed to SMSFs paying TRISs. Within APRA-regulated funds, the removal of tax exemption from TRISs from 1 July 2017 created addition transaction costs, including potential CGT issues when shifting to the retirement phase, which would have been as an Account Based Pension (ABP).

The policy response was therefore to introduce the concept of a TRIS in retirement phase to ensure that an individual didn’t incur costs in moving their benefits into a tax exempt environment. For SMSFs, this transaction cost doesn’t exist as the product (income stream) paid under SIS Regulation 1.06(9A) still remains and is argued amongst professionals within the industry that it can be restated as an ABP (a view we share). Unfortunately, it’s not a view shared by the ATO, so we move forward under these terms.

Key differences

It is important to note that there are a few differences between a TRIS and TRIS in the retirement phase – we have highlighted some of these below:

| TRIS in the Retirement Phase | TRIS not in the retirement phase |

| the earnings from the assets supporting the TRIS will be eligible for ECPI, and | the earnings from the assets supporting the TRIS will not be eligible for ECPI, and will be taxed at the relevant tax rate, and |

| it will be counted towards the member’s transfer balance cap. | it will not count towards the member’s transfer balance cap (until it goes into the retirement phase). |

| Is counted towards the member’s retirement phase value for total superannuation balance purposes | Is counted towards the member’s accumulation phase value for total superannuation balance purposes |

| Subject to the fund’s deed and terms of the income stream, the 10% maximum and commutation restrictions fall away upon a condition of release (with nil cashing restriction) being met | SISR 6.01 applies, providing a 10% maximum and restrictions for any commutation of the income stream |

Importantly, earlier this year, the legislative anomaly was fixed with the reversionary status of a TRIS – you can read more about this in a previous blog post, Reversionary TRIS legislation now fixed.

So when can a TRIS become an ABP?

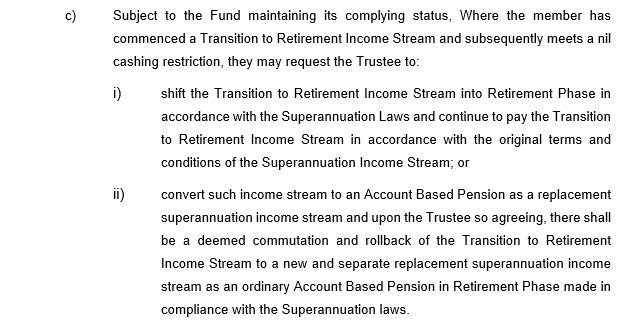

It is the ATO’s view that an ABP will only be created where a TRIS ceases. It is therefore a conscious decision that needs to be made via a commutation and re-purchase of the income stream. Therefore, the member is going to have to consider whether they wish to continue with a TRIS, into the retirement phase, or alternatively commute and repurchase as an ABP. Rule 25.1(c) of the Smarter SMSF Deed provides the choice for a member to request the Trustee to either shift the the TRIS to retirement phase or alternatively create a replacement income stream, by triggering a commutation and rollback.

Smarter SMSF Deed – Rule 25.1(c)

It is important to note the makeup of a member’s superannuation interest(s) with any commutation and repurchase given that a SMSF member will only ever have one accumulation phase interest.

Just because the law says…

Where a member satisfies a condition of release set out in s.307-80 of the ITAA 1997 to move the benefit to the retirement phase, the TRIS Regulations within SIS 6.01 allow for the cashing restriction (of preservation) and the 10% maximum pension to ‘fall away’. Whilst the legislation may allow for this to occur, it is important that you also understand what the terms of the trust deed and pension say about the ability to remove any maximum pension restriction with a TRIS. For example, we have seen trust deeds where the TRIS definition prescribed a maximum of 10%, effectively meaning that any member where a condition of release is satisfied (e.g. reaching age 65) and the benefit moves to retirement phase, will still be subject to a 10% maximum until the governing rules are altered.

As a result, there are some important decisions to be made at the time when converting to retirement phase and having the account balance count towards a member’s transfer balance cap (TBC). Having the right documentation in place forms an important part of this process.

You can read more regarding the release of GN 2019/1 on the ATO legal database.

Order your TRIS documents a smarter way

To support this view by the ATO, Smarter SMSF provides the following pension documentation regarding Transition to Retirement Income Streams:

- Pension Commencement

- TRIS to Retirement Phase

- Add or remove a reversionary beneficiary